If you ever consider rebalancing your private equity allocation, the time is now. As a result of record amounts of capital committed to private equity secondary funds, active portfolio management on private equity funds is as cheap as ever. It’s a bold bet that conditions will stay this favorable forever.

In this short research note we discuss a number of broad market indicators that show the attractiveness of the private equity secondary market, with a particular emphasis on a seller’s point of view. Of course actual fund-specific pricing can deviate substantially from these averages. Some sought-after names are trading above NAV, while some tail-end fund can trade at half their account value. This price differentiation is reflecting the massive quality differences across funds.

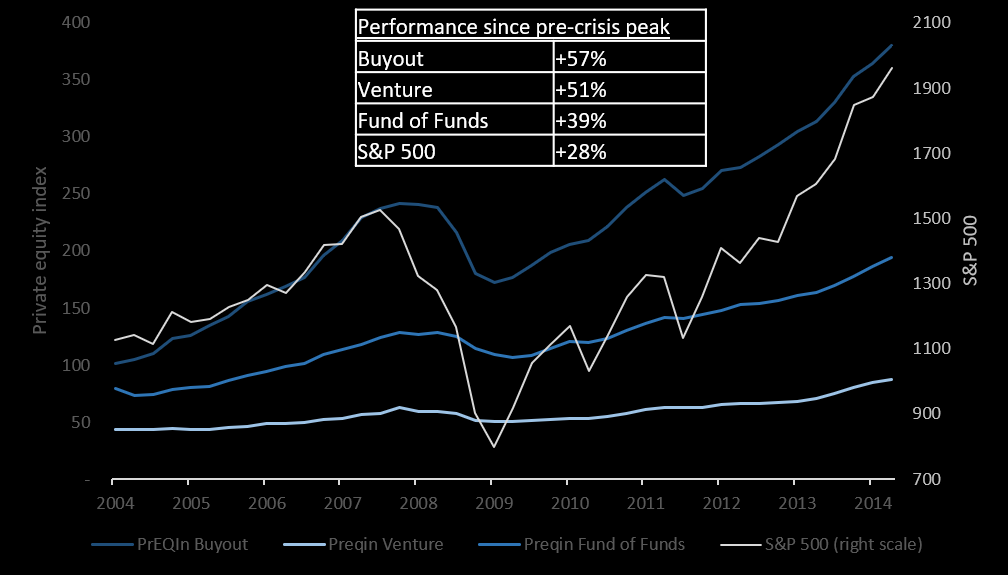

Let us start with a general performance review of the three private equity sub-sectors buyout, venture and fund-of-funds. We examine the performance development graphically and calculate the return from the pre-crisis (2004 to 2007) highs until today.

Figure 1: Performance indices for average private equity fund, 2004 to 2014; source: Preqin, Bloomberg

Clearly, the average private equity fund has created substantial performance, not only on an absolute basis but also compared to the public equity market.

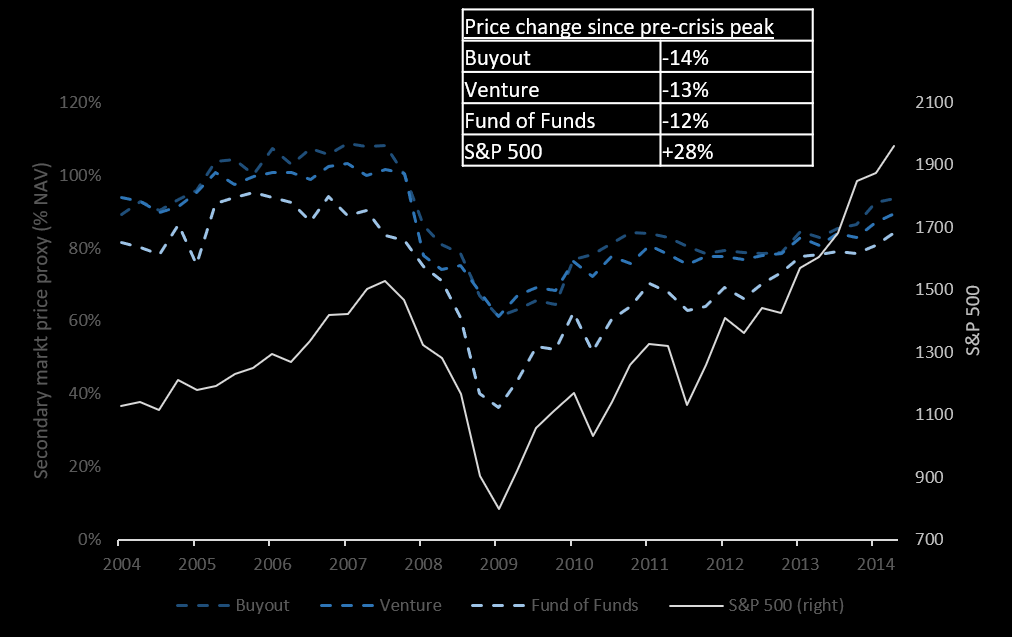

Secondary market pricing, in percentage of NAV, are up 50% to 60% since the bottom of 2009. Looking back further, we are still below the all-time-highs seen in 2007 though.

Figure 2: Secondary market pricing proxy index, source: Multiplicity Partners’ calculation using various publically available and internal data sources

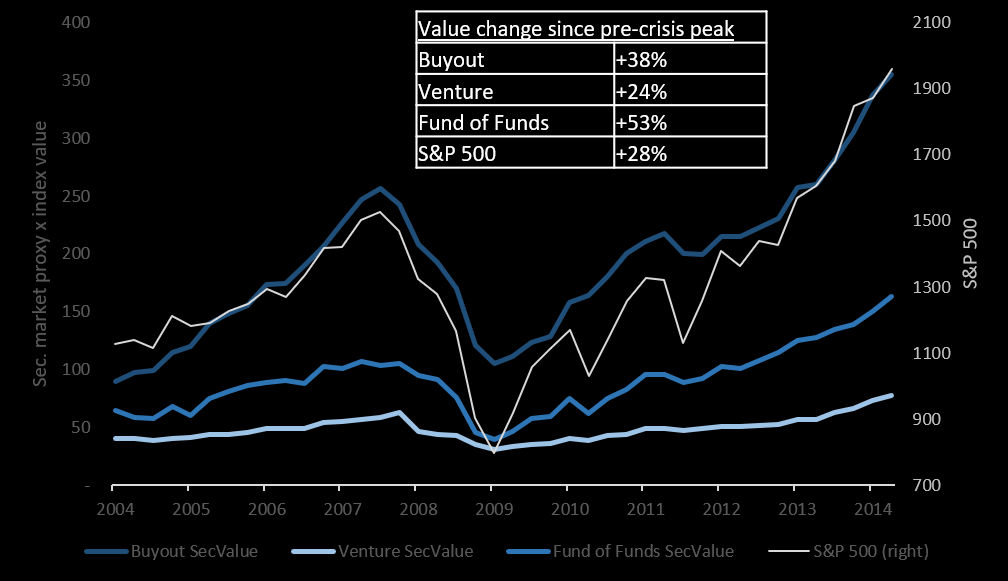

We now combine the performance data with the secondary pricing index to calculate a “secondary value” index.

Figure 3: Secondary market proxy value index, source: Calculated using Preqin’s performance index and Multiplicity Partners’ secondary pricing proxy

This last chart evidently shows that the market currently offers a great opportunity to realize profits since both NAVs and secondary prices have appreciated substantially over the past few years. If you wish to discuss potential private equity divestments resp. portfolio rebalancings, please do not hesitate to contact us.