There is no such thing as a passive investment in private markets. Investing in private assets must be based on active decisions, and choosing a good General Partner is of paramount importance.

That also holds true for private credit. In our view, there is hardly an investment strategy where investment skills, or underwriting quality, is more important.

Of course, you can be lucky, and all your private loans get repaid because the economy is strong. However, delivering good results, in the long run, is less likely the result of chance than for other strategies.

In our piece, we will first look at how COVID-19 has served as a catalyst to separate private debt managers into the ‘good’ and the ‘ugly’. In the second part, we focus on open-end funds in the segment.

Luck or skill?

Venture capital, and at times also private equity, are notorious for luring investors into mistaking luck for skill. In our deal sourcing, we regularly come across many a stellar track record, only to find out that it got skewed by a single lucky outlier transaction that resulted in a 32X. In some cases, a fund manager may have found the proverbial ‘bigger fool’ to offload an asset before the bubble bursts.

As our analysis will show, luck is less likely to help private debt managers. Quality is everything.

Since there is limited transparency on private market credit funds, we analysed their listed counterparts to obtain a representative overview of the private credit space.

As a proxy, we took the Indxx Private Credit Index, which tracks the performance of Business Development Companies (BDCs) and certain Closed-End Funds trading in the US. If you look at their London-listed counterparts, the picture is very similar. Take a look at, e.g., the DLX Index by LPX.

Why BDCs are a good proxy for private credit funds:

Business Development Companies are lending to small and mediums sized companies in the US, many of which happen to be privately funded as well. It should therefore not come as a surprise that BDCs are managed to a large part by the same managers/GPs that manage private debt funds.

As the first wave of COVID-19 ignited fears about the potential impact on the economy, the Indxx Private Credit Index lost almost 50% in March but continues to recover since.

Figure 1: Indxx Private Credit Index, data as at 11 September, 2020; source: Bloomberg

Similar to the equity markets, this index does not reveal the whole picture, particularly in event-laden years like 2020.

What valuation to trust

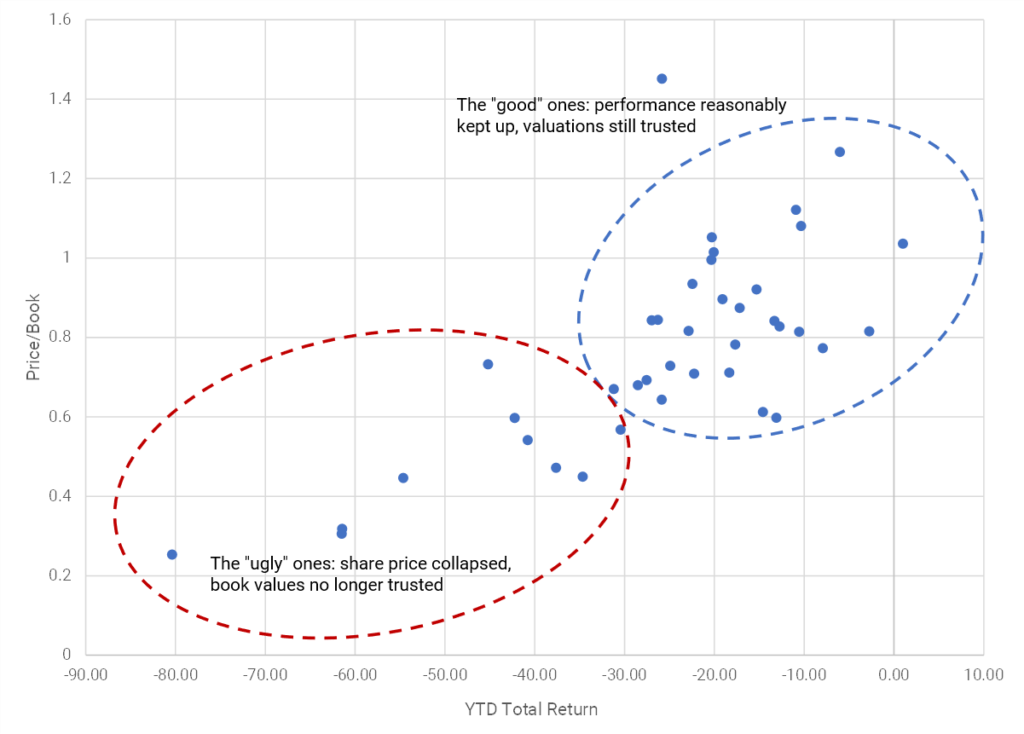

If one plots the year-to-date returns of the index constituents against their respective price-to-book ratio, it becomes clear that COVID-19 has served as a catalyst to separate the wheat from the chaff in the private credit universe.

Figure 2: Indxx Private Credit Index, year-to-date returns of the index constituents against their respective price-to-book ratio, data as at 11 September, 2020; source: Bloomberg

Conservative investors may be particularly vulnerable

Traditionally, conservative investors used to look towards fixed income for stable, predictable yields.

Given the record low interest rates, many have started investing in increasingly exotic credit, thereby loading up on overpriced yield and uncomfortably high levels of risk. This has not only happened in public markets but also increasingly in private credit markets.

That said, we generally appreciate the merits of dis-intermediation. Non-bank lenders will undoubtedly lead to a more diverse and efficient capital market that, in the long run, will benefit everyone involved. No doubt, many institutional private debt players navigate this new space well. We may be about to find out soon who does not.

Private credit funds with regular liquidity – a recipe for disaster?

As you may be aware, Multiplicity Partners is active both in private market fund secondaries and in distressed assets. Occasionally, we find ourselves at the intersection of these two areas.

For years, we observed an increasing number of private debt niche strategies, such as factoring, trade finance or P2P lending, being offered as open-end funds to relatively inexperienced but yield-hungry investors. We became more and more concerned about the liquidity mismatches and underwriting standards of this particular breed of private credit funds.

This is why we are so concerned watching relatively inexperienced investors pile into open-ended private credit funds, trade finance, or online P2P lending platforms in recent years.

Our suspicions were confirmed already last year as several open-end private credit funds had to apply redemption gates, suspended redemptions altogether, or even came under the scrutiny of the US Securities and Exchange Commission (SEC).

We believe that these instances are only the first symptoms of a far-reaching crisis. We anticipate a significant surge in private credit funds to fall into distress, and, with some delay, also some closed-end funds.

The canary in the coal mine

Since last year, we are coming across some very nervous private credit fund investors. Sitting on fund interests with supposedly quarterly liquidity, they have been waiting for months for their redemptions to go through.

Redemption gates might be only the beginning of a severe liquidity problem across the segment. We would not be surprised to see a chaotic run for the exits, as the remaining investors realize their open-end credit fund investments were anything but liquid.

Except for the occasional fraud story, googling for ‘private credit crisis’ or similar will not offer the expected wave of alarming search results. Are we crying wolf, or is there something else at play?

Kicking the can down the road

Many investors are very reluctant to admit to, or even talk about, being exposed to non-performing credit. Even before Covid-19, we experienced this first-hand as we approached lending platforms to get a better understanding of their non-performing loans.

Funding Circle, one of the leading global lending platforms, still quotes creditor default numbers in the 2.1% to 4% range (https://www.fundingcircle.com/uk/statistics/). They do, however, note that those estimates are correct as at 31 December 2019 and do not include any potential impact of COVID-19.

Given our market observations, we believe these figures to be way too optimistic for the broader market in the medium- to long-term.

It appears that, at least partially out of self-interest, some platforms might be artificially keeping defaults low by applying rather creative marking-to-market practices. By allowing their creditors to kick the can down the road and rolling their debt, these platforms keep earning fees, thus inflating their corporate valuation.

The dirty little secret of the open-ended private credit fund segment

Professional investors with non-performing credit exposure on their books appear to be keeping the ball low as well, fearing that speaking up might send the market into a free-fall, thus destroying any prospect of them recovering their principal. Not to mention the resulting dressing down by competitors.

Watching private credit secondaries go bad

While we have seen a massive surge of inquiries for secondaries on private credit funds (particularly on open-end funds that were sold with regular redemption rights), only a few trades have been executed so far. The gap in price expectations between sellers and buyers still seems unsurmountable.

Private debt funds on the radar of the SEC

It appears that the US Securities and Exchange Commission (SEC) is stepping up the scrutiny of private debt schemes.

A Reuters article at the height of the first COVID-19 wave in early March 2020 mentions concerns about the amount of money pouring into them, increased risk in their loans, and room for pricing manipulation, especially in a recession. The article goes on to quote an unnamed SEC source with “We’ve had a lot of concerns over private lending.”

A seller’s journey – from identifying the problem to getting their price expectations in line with the market consensus

Let us illustrate this multi-faceted journey that can easily take more than a year with an example:

Imagine you were just informed that your fund can’t honour your redemption and has to apply some gating. Your initial optimism quickly yields to scepticism as you learn that the fund is going into liquidation because most other investors want to get out.

Shortly after that, you start to hear about “isolated” issues with some credit positions.

And from here on, things go down-hill. The fund’s liquidators inform you that they will have first to repay credit lines used for leverage.

To make matters worse, you might learn that there was outright fraud involved. This is what happened to investors in Princeton Alternative and Direct Lending Investments, two prominent cases that unraveled during the last two years.

All of this has to sink in before a seller might emotionally come to terms with a price that any reasonable secondary buyer would be prepared to offer.