It’s a sellers’ market for distressed assets, across troubled bonds, bankruptcy claims and NPLs.

Record amounts of dry powder keep pricing extremely firm.

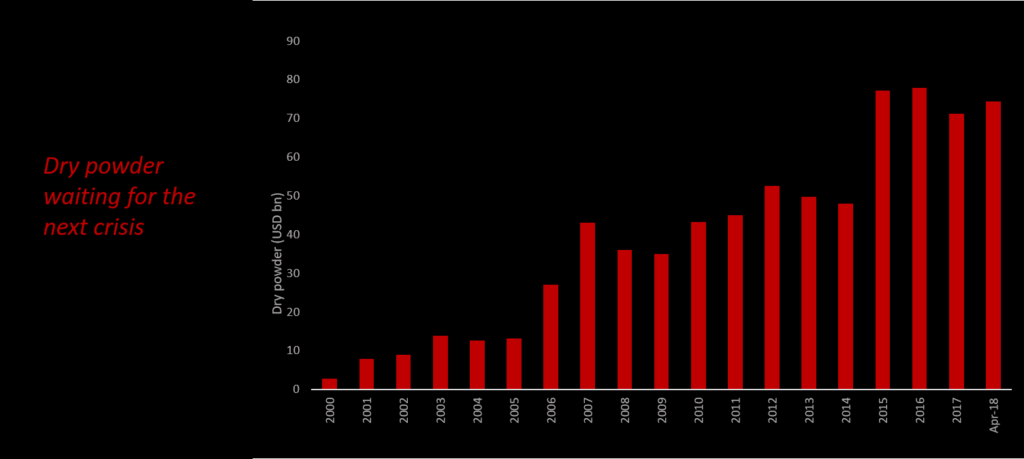

Waiting for the next crisis

In anticipation of the next credit crunch investors have piled into distressed funds over the past few years. Is it the inevitable turn of the interest rate cycle, the bursting of a bubble, or a political shock that will trigger the next big downturn? No one knows for sure. We do know, however, that chance favours the prepared. We believe that is why so much capital has been allocated to distressed funds recently, and demand for distressed investment opportunities is as big as ever.

Figure 1: Dry powder in distressed debt funds, 2000 to April 2018; source: Preqin

Reorganisations in the US, non-performing loans in Europe

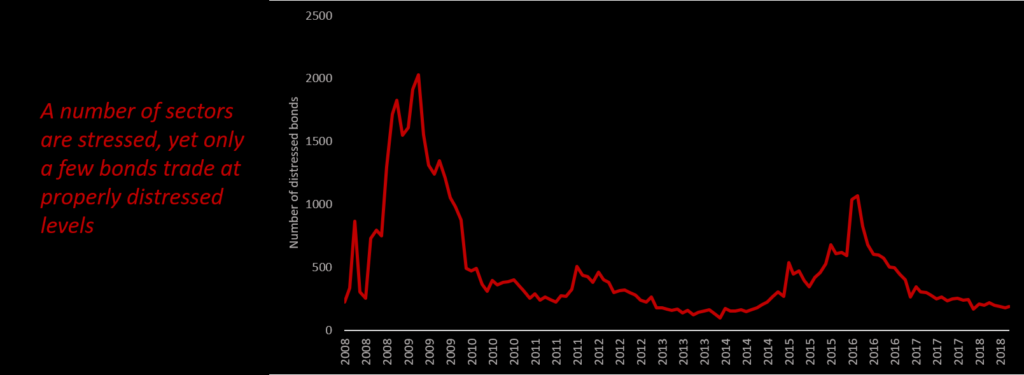

To gain a better understanding of the opportunities, we look at the supply side and the various segments of distressed markets. In the US, we observe distressed investing predominantly around Chapter 11-related reorganisations, with most of the action in the energy, and now also increasingly in the retail sector.

Figure 2: Number of bonds traded at yields greater than 1000bps above benchmark treasuries; source: Bloomberg

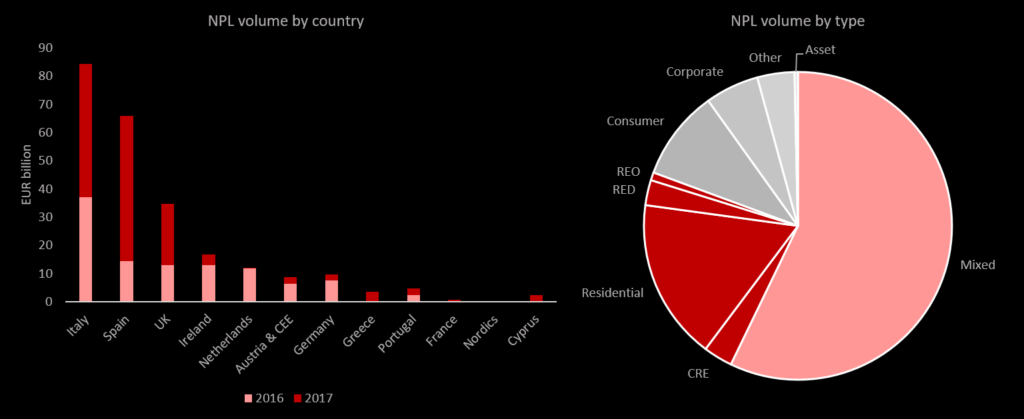

In Europe, non-performing loans (NPLs) are by far the most relevant distressed market. While Italy is in the spotlight now, the attention of the NPL market shifts across countries year-by-year, depending on where they are in coping with banking legacy issues. Pan-European investing in NPLs is a difficult task, however. Local rules differ substantially across jurisdictions, and some legal systems appear to favour insiders and local players. Real estate-backed loans are seeing the largest deal volumes, regardless of jurisdiction.

Figure 3: European NPL activity; source: Deloitte

In China and India, we are only starting to see banks face pressures to clean up their balance sheet and bring their overdue loans to the market. These two countries probably make up the bulk of the next wave of supply. Shipping is a sector that Multiplicity has specifically covered for the past five years. Many segments of the container market in particular still suffer from a massive oversupply of ships and charter rates at unsustainably low levels. This will keep delivering potential distressed purchase opportunities for some time.

Dreaming of double digit returns

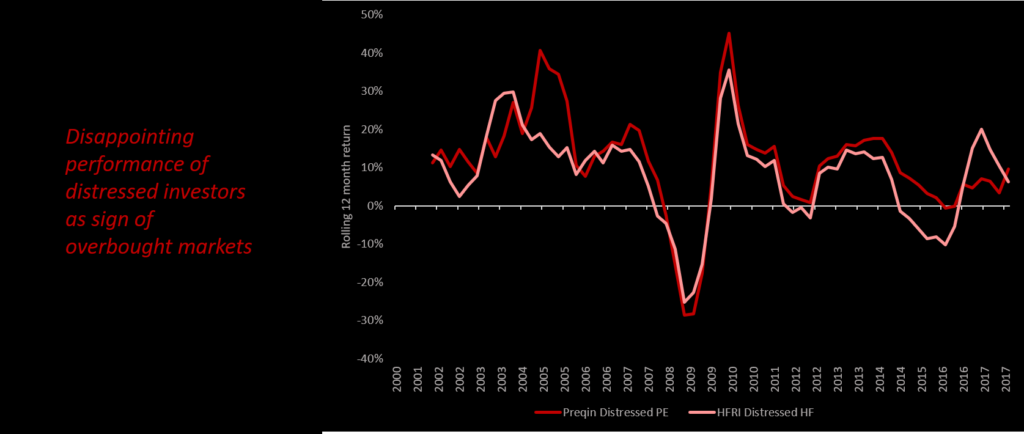

While most areas of the distressed market have become more intermediated and transparent, any meaningful pricing data is still hard to come by. In the US, any sizable reorg opportunity is highly competitive. To some degree, this is reflected in Figure 2 showing only few bonds trading at yields above 10%. Another way of looking at this is the performance of distressed private equity funds (typically control-oriented and more longer-term) and hedge funds (typically as minority investors with limited control). The subdued performance can well be interpreted as an indication that investors overpaid for distressed assets.

Figure 4: Rolling 12-month net returns of distressed private equity and hedge funds; source: Preqin Distressed Private Equity Performance Index, HFRI Distressed

In the European NPL market we note that some parts have been flooded with money from non-traditional buyers, e.g. large institutional investors, family offices or servicers that have lower yield targets. Realistically, most larger transactions will not be underwritten with double-digit IRR targets, and if so, only because of less-than-realistic recovery assumptions.

Leverage returns to the stage

Another factor that keeps pricing firm is the re-emergence of leveraged buyers. It’s again possible to lend against less liquid assets. Remember how banks used to avoid this practice after the financial crisis of 2008?

Whatever your motivations to consider a sale of some of your distressed positions, do not hesitate to contact us for an indicative pricing. Please write to Thomas today at tr@mpag.com, or call him at +41 44 500 4553.