Many investors find themselves with private equity fund interests that are well past the life span stated in the limited partnership agreement (LPA).

Imagine if there were a simple and fast method to determine the ‘fair’ price for such mature private market funds across the quality spectrum.

The framework is intentionally simplistic in order to provide a good starting point for both buyers and sellers to determine the fair price such limited partnership interests should realistically be able to command in the secondary market today. One must, however, account for idiosyncratic risks in each fund, and understand the economic context.

The market is full of funds well past their intended life-span

If one is to believe many traditional LPAs, then private equity funds are supposed to wind down after ten years. It is increasingly becoming an exception that they liquidate within this intended life span.

Granted, there are often built-in extension periods (e.g., two additional one-year terms) to efficiently liquidate the underlying portfolio holdings. One might think that this would present ample time to get rid of residual positions.

A recent study of PitchBook found however (see figure 1 below) that the average private equity fund duration (i.e., the time a fund takes to fully liquidate) is now exceeding 12 years, and even fund durations of 15+ years have become quite common.

The LPA may say ten years, but private equity fund durations of 15+ years have become quite common.

Most private equity funds are past their intended life

Figure 1: Number of PE funds to fully liquidate by quarter since inception, data as at 31 December, 2018; source: PitchBook

Funds that perform in year five tend not to disappoint in year 12.

Can thousands of financial product disclaimers possibly be wrong?

If there’s anything investors remember from reading product disclaimers, it’s that past performance is no indication for future results. Nevertheless, there’s a common perception that a fund’s past performance provides at least some level of guidance to future performance.

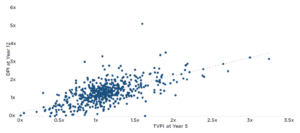

PitchBook’s recent analysis found a strong correlation of 0.65 between funds’ 5-year total value to paid-in (TVPI) and their respective distributions to paid-in capital (DPI) in year 12.

There is a strong correlation between early and late-stage performance of the same fund

Figure 2: Private equity fund TVPI at year 5 vs DPI at year 12, data as at 31 December, 2018; source: PitchBook

A top-quartile fund should be worth substantially more in the secondary market compared to a bottom-quartile peer.

Good funds keep outperforming, laggards keep disappointing

Let’s delve a bit more into the topic of ‘fair’ secondaries pricing. At Multiplicity, we focus on mature (or even tail-end) secondaries; hence the reason we used a data set from Preqin that grouped 8 to 9-year-old funds into performance quartiles and then looked at their future distributions.

Of course there is variation across funds within each of these quartiles buckets, but on average, the pattern is pretty constant over time: good funds continue to outperform, laggards continue to disappoint.

Rule of thumb: a top-quartile fund should trade at a 42% premium to its net asset value

Let’s now make the heroic assumption that all secondary buyers are looking to achieve a target multiple of 1.6x (as per Preqin’s recent surveys, the average number should be around there).

Using historical distribution patterns of our mature (i.e., 8-9 years old) private market funds, let’s then calculate the ‘fair’ secondary price by dividing these funds’ cumulative future distribution by 1.6. The average top-quartile fund distributed between 176% and 252% of their year 8-9 net asset value (NAV), with the long-term average being 227%.

A bottom-quartile fund’s ‘fair’ price should be at a 62% discount to NAV.

Using the 1.6x ‘fair’ multiple, a top-quartile fund should trade at a 42% premium to its NAV! At the other end of the spectrum, a bottom-quartile fund’s ‘fair’ price would be just 38%, which is a 62% discount to NAV.

‘Fair’ secondary prices assuming an expected multiple of 1.6x

Figure 3: Calculated ‘fair’ secondary prices of private equity funds across quartiles, assuming an expected multiple of 1.6x; source: Preqin, Multiplicity Partners

Rule of thumb: top-quartile funds should trade at double-digit premiums, while bottom-quartile funds should trade at 50%+ discounts

We agree that the above framework is simplistic and there are major idiosyncratic risks in each fund (aside from the need to understand where one stands in the economic cycle), but we still think the numbers presented are a good starting point: top-quartile funds should trade at double-digit premiums, while bottom-quartile funds should trade at discounts of 50% and above.

Those fixated on the NAV will consequently, and unfortunately, let go of their best funds at NAV.

Rule of thumb: sell your bad fund, even if it’s at a considerable discount to its book value

Our observations of the secondary market showed that sellers tend to be fixated on pricing relative to NAV. This could explain why they tend to have their best funds picked up at a price around NAV. Realistically they would be much better off selling bad funds, even if it’s at a massive discount to their book values.