In this article, we conclude that the private equity secondary market is as strong as ever and that there are even suitable buyers for fund sizes below USD 1 million. With public and private equity markets at all-time highs and dry powder at record levels, we argue that now is as good as ever to consider a sale of LP interests.

The market seems to know only one direction – up

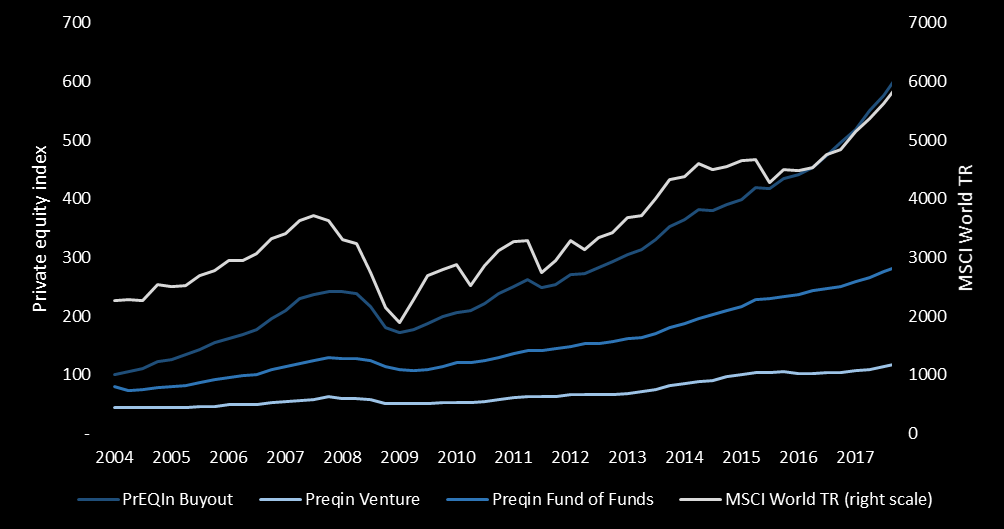

The so-called Trump bump, with stock markets ending 2017 at all-time highs, was also reflected in the valuation of many private equity funds.

Both public and private equity market proxies continue to reach all-time-highs.

Figure 1: Performance indices for average private equity fund, 2004 to 2017; source: Preqin, Bloomberg

In this article, we conclude that the private equity secondary market is as strong as ever and that there are even suitable buyers for fund sizes below USD 1 million. With public and private equity markets at all-time highs and dry powder at record levels, we argue that now is as good as ever to consider a sale of LP interests.

The run on private equity since 2009 has led to an increase in dedicated secondaries players. It has also attracted non-traditional investors such as pension funds and insurance companies.

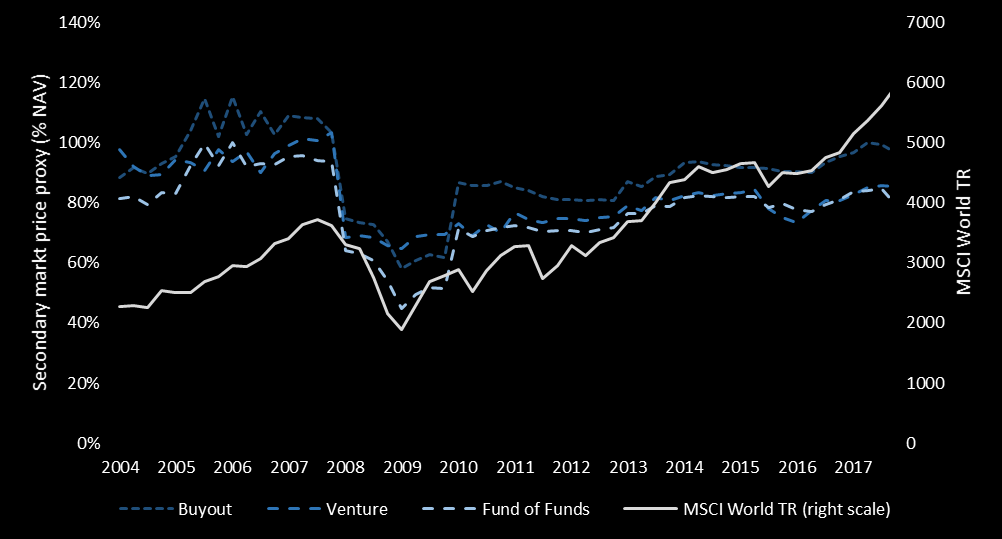

Non-traditional buyers drive up secondary pricing..

We estimate that average discounts to NAV for buyout and venture funds narrowed by 3 to 5 percentage points in 2017. As target multiples for most secondary fund managers remained unchanged in the range of 1.3x to 1.8x, pricing seemed to be driven up by non-traditional buyers. While this group of buyers tends to be less informed than the secondaries specialists, they have substantially lower costs of capital.

Avg. discounts to NAV for buyout and venture funds are down to 3-5 percentage points.

Figure 2: Secondary market pricing proxy index; source: Multiplicity Partners’ calculation using various publicly available and internal data sources

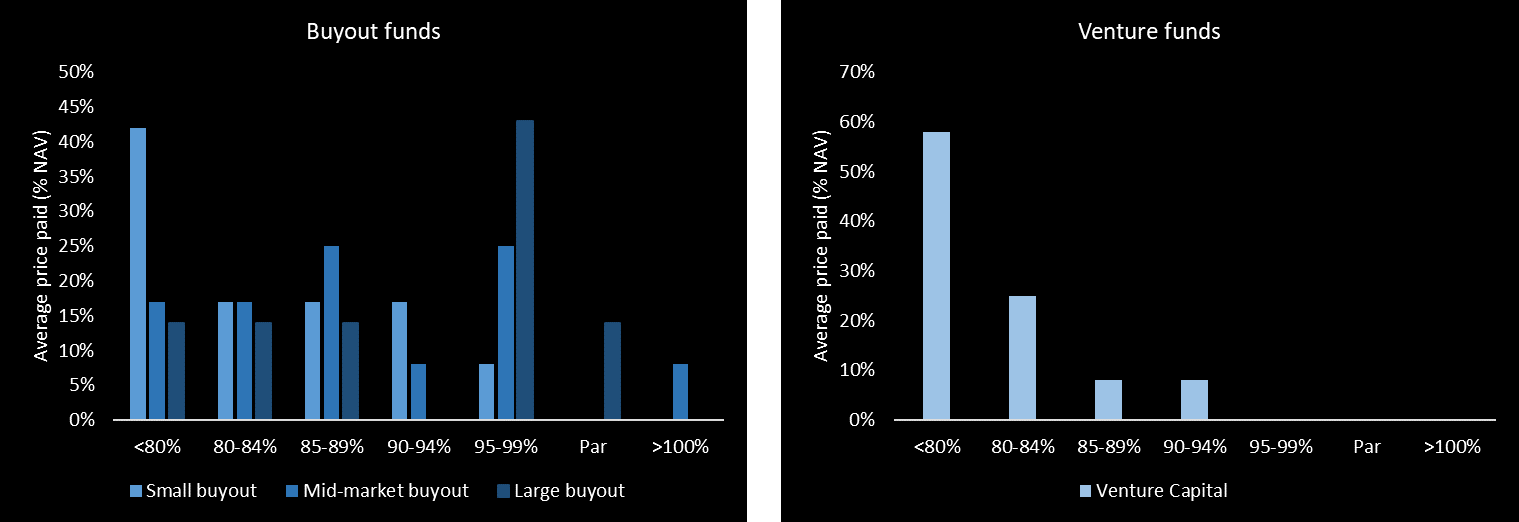

..and yet, many assets trade at discounts well above 20%

Let us take a closer look at the price dispersion within the buyout and venture space. The aggregate pricing proxy is not revealing the whole truth. Many underperforming and less sought-after names are still trading at discounts well beyond 20%.

Figure 3: Average price paid for secondaries in 2017; source: Preqin secondary fund manager survey

It might be a good time to sell some private equity..

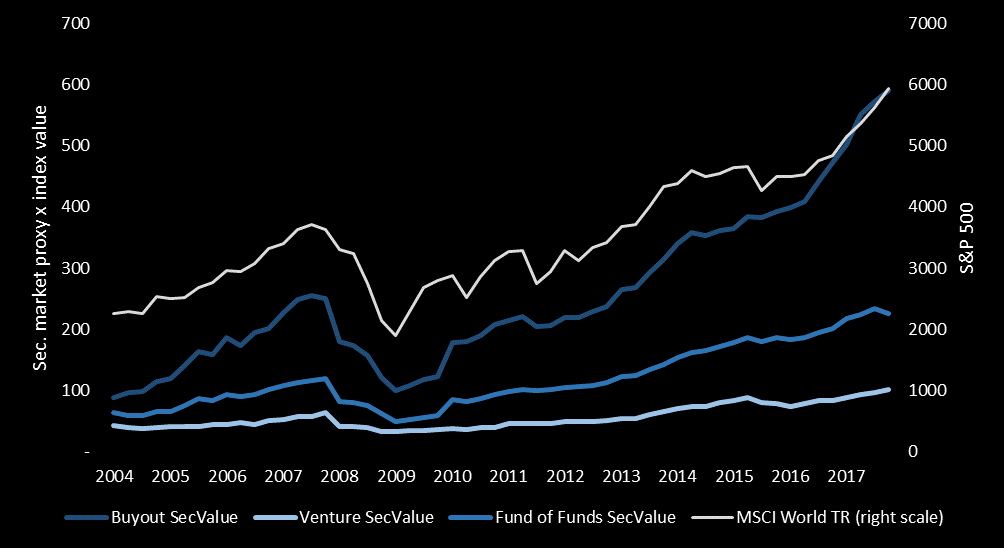

As a measure of absolute value in the private equity secondary market, we combine the private equity performance data (Fig. 1) with the secondary market pricing proxy index (Fig. 2) to calculate a Secondary Market Value Index. No surprise here: we also observe record pricing levels on this chart, and it seems a good time to consider a sale of your private equity holdings.

Our proprietary Secondary Market Value Index shows record pricing levels.

Figure 4: Secondary Market Value Index; source: Calculated using Preqin’s performance index and Multiplicity Partners’ secondary pricing proxy index

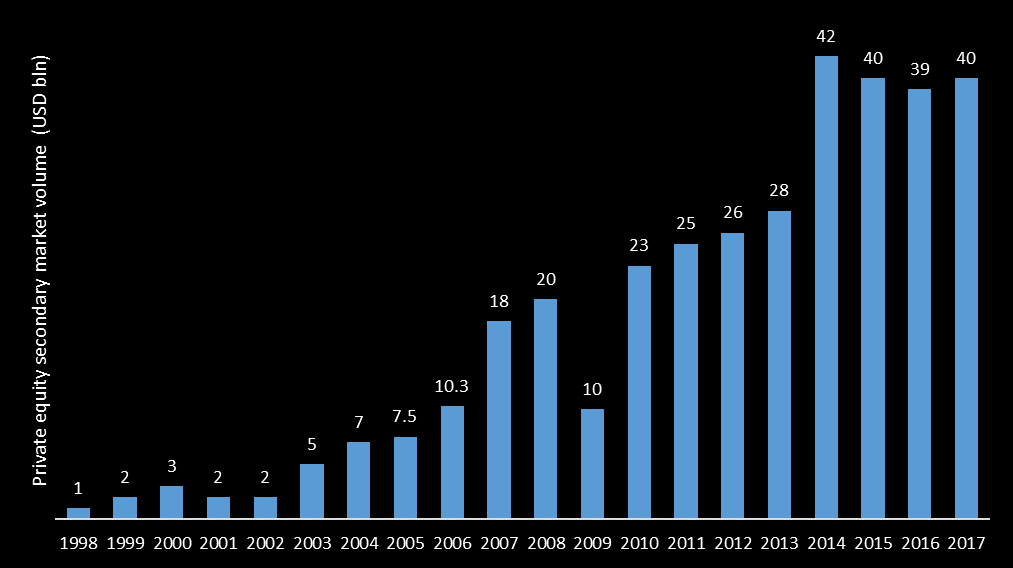

..as the secondaries market shows robust volumes, and sufficient depth and breadth

According to data provided by large intermediaries, transaction volume seems to have stabilized around a level of approximately USD 40 billion in 2017. If we compare this number to the overall size of the private equity industry, which is estimated to be between USD 2.5 to 3 trillion, we observe an annual turnover of merely 1.5%.

Global annual secondaries turnover is only 1.5%.

Figure 5: Global private equity secondary market volume; various sources

There are specialized buyers even for sizes below USD 1 million

We believe the low relative amount of turnover in private equity holdings is not particularly meaningful. Today any private market fund interests can be sold competitively. There are a sufficient number of specialized buyers in any market segment, be it private equity, real estate, infrastructure, tail-end situations and for sizes of below USD 1 million to USD 1 billion+. According to Preqin, dedicated secondaries funds held USD 89 billion of dry powder in December 2017, which is only slightly down from the previous quarter’s all-time record of USD 94 billion. The stable volumes combined with growing demand is keeping pricing firm.

Would you like to receive a quick indicative pricing for your asset? Or share your views on this article? Please write to Andres today at ah@mpag.com, or call him at +41 44 500 4555.